CIBIL Score Below 730? What RBI's New Home Loan Rules Mean in 2027

A difference of ₹4.6 lakh. That’s roughly what a weak CIBIL score could add to a ₹50 lakh home loan from April 2027 — not through rejection, but through a higher interest rate the bank quietly charges you for being a bigger risk.

The RBI has finalised a new lending framework that goes live on April 1, 2027. It changes how banks measure credit risk on every loan they give out. For borrowers below a CIBIL score of 730, the change has a direct price tag. For borrowers already above 750, things might actually get slightly better.

Here’s what’s changing, what it costs in rupees, and what to do before the deadline.

What’s Changing in April 2027

Right now, banks set aside money for bad loans only after a borrower stops paying. They wait for the problem.

From April 2027, that changes. Under the new Expected Credit Loss (ECL) framework, banks must estimate which loans are at risk of going bad — and set aside funds from the day the loan is sanctioned. The riskier a borrower looks, the more money the bank must hold in reserve.

That changes the economics of lending to borderline borrowers. Banks will either price the risk into your interest rate, ask for more collateral, or decline the application.

The 730 Number: Where It Comes From

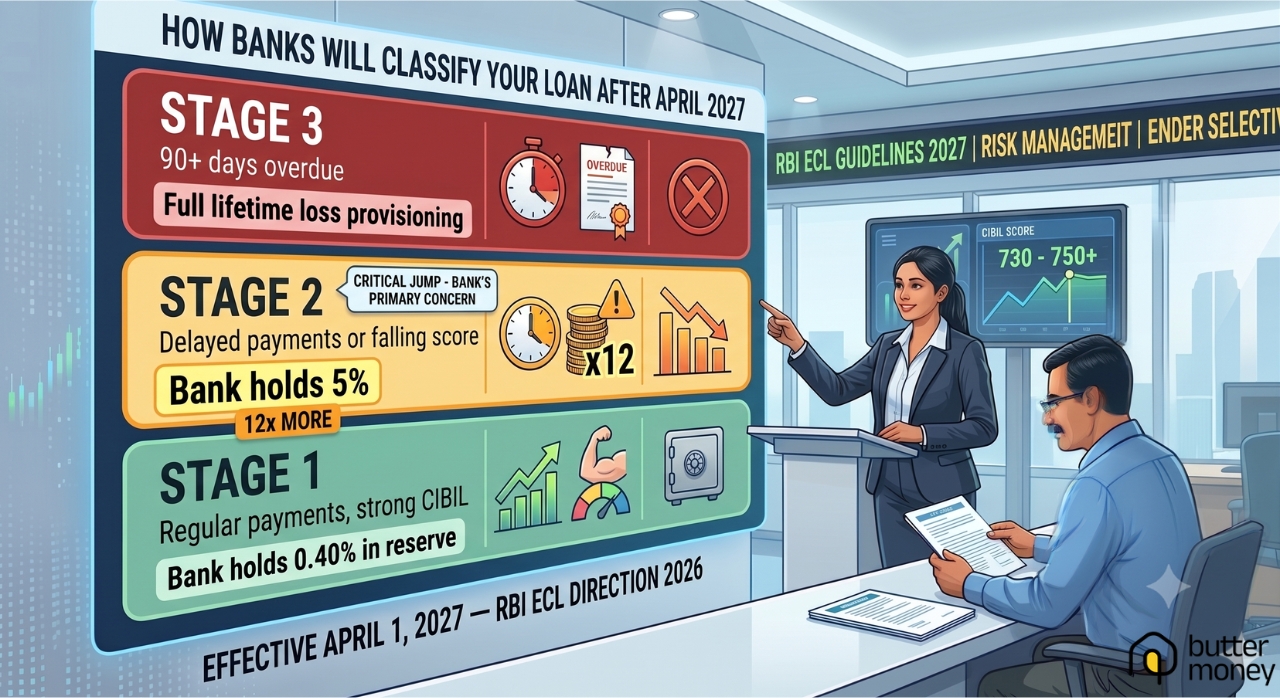

Every loan under the new system gets classified into one of three stages:

Stage 1 — Low risk. Regular EMIs, strong CIBIL score. Bank sets aside 0.40% of the loan. Same as today, no change for clean borrowers.

Stage 2 — Elevated risk. Payments are 30 to 89 days late, or the bank sees early warning signs like a falling CIBIL score. Bank must now set aside a minimum of 5% of the loan amount. That’s more than 12 times the current requirement.

Stage 3 — Defaulted. 90+ days overdue. Bank provisions for full lifetime losses.

The Stage 2 jump is the one banks are nervous about. To avoid it, they’ll be more selective at the application stage about anyone who looks like they might drift from Stage 1 into Stage 2.

A CIBIL score below 730 puts a borrower closer to that boundary in the bank’s internal risk model. It’s not an RBI rule — it’s a risk management threshold most lenders are expected to use. According to industry estimates, around 7 crore borrowers in India currently have scores of 730 or above. The majority of active credit users sit below that mark.

What a Lower Score Actually Costs You

Use the Butter Money EMI calculator to run these numbers for your specific loan amount.

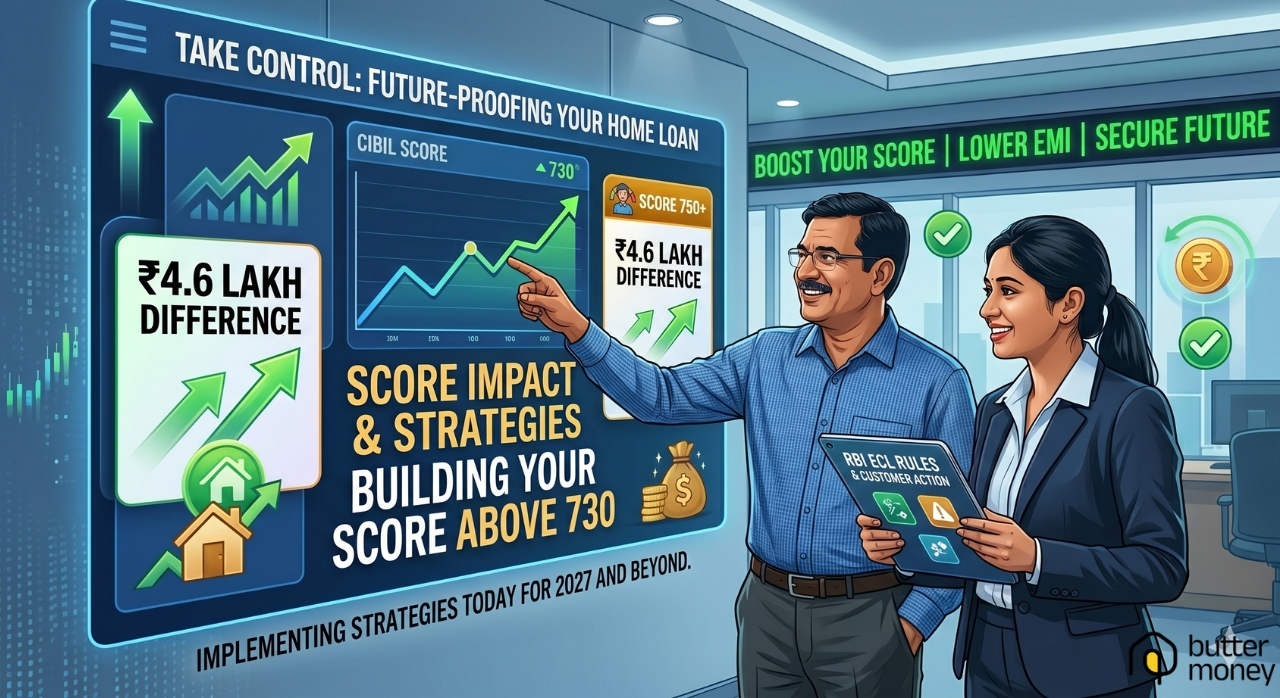

Here’s a straightforward example. A ₹50 lakh home loan over 20 years. A bank charges a 0.50% risk premium for a borderline CIBIL score. That’s a conservative estimate — the actual spread could be higher depending on the lender.

| Score 750+ | Score 680–720 | |

| Interest rate | 8.75% p.a. | 9.25% p.a. |

| Monthly EMI | ~₹44,200 | ~₹46,100 |

| Total interest paid | ~₹56.1 lakh | ~₹60.7 lakh |

| Extra paid over 20 years | — | ~₹4.6 lakh more |

On a ₹75 lakh loan over 25 years, the same 0.50% premium adds over ₹8 lakh.

The bigger the loan and the longer the tenure, the more expensive a borderline CIBIL score becomes — and this is before factoring in lenders who might charge 0.75% or 1% more rather than 0.50%.

What Banks Will Actually Look at Beyond Your Score

The ECL model doesn’t run on CIBIL score alone. Banks will assess a combination of:

- Income stability — A salaried employee with consistent increments scores better than freelance income at the same level, because the probability of default is calculated differently

- Existing EMI load — If existing EMIs already take up more than 50% of your take-home pay, risk flags go up. This is called FOIR (Fixed Obligation to Income Ratio — the share of your income already committed to debt)

- Loan-to-value ratio — The more you put in as a down payment, the less the bank needs to hold in reserve against your loan

- Repayment patterns — Not just whether you’ve defaulted, but how close to the due date you typically pay. Paying on the last day is not the same as paying two weeks early in a risk model

A borrower with a 735 CIBIL score but high existing debt and variable income may still face tighter terms. A 715-score borrower with stable income, low existing EMIs, and a 30% down payment may find lenders willing to work with them.

Understand how FOIR affects your home loan eligibility — complete guide on Butter Money

When This Change Won’t Affect You

Not everyone needs to act. The ECL norms are unlikely to change anything for you if:

- Your CIBIL score is already above 750 with a clean repayment record

- You’re putting in 30% or more as a down payment

- Your existing EMI obligations are under 40% of take-home income

- You already have a home loan and are paying it on time — ECL doesn’t let banks retroactively change terms on a performing loan

Also worth knowing: 730 is not an RBI-mandated cutoff. It’s an industry estimate of where banks will draw the line internally. Some housing finance companies may continue lending below that threshold but typically at higher rates.

How to Improve Your CIBIL Score Before April 2027

Nine months is a workable window. Here’s what to actually do:

- Pull your CIBIL report today. Check for errors — wrong addresses, outdated defaults, accounts you didn’t open. Disputes take 30 to 60 days to resolve. Start now, not in December.

- Set auto-pay on every credit account. Payment history drives your score more than anything else. One missed due date can knock 30 to 50 points off immediately.

- Get credit card utilization below 30%. Using ₹80,000 of a ₹1 lakh credit limit looks like financial stress to a lender. Pay it down to under ₹30,000.

- Stop applying for new credit. Every application triggers a hard enquiry on your CIBIL report, which dips your score and signals to lenders that you’re reaching for credit.

- Keep old credit cards open. Age of credit history is a scoring factor. An unused card with zero balance and no annual fee is an asset, not a liability.

Six to nine months of clean behaviour typically moves a score from the 650–700 range to above 730. Not guaranteed, but predictable.

If Your Loan Is Happening Around the 2027 Window

A few specific points if you’re planning to apply for a home loan in late 2026 or early 2027:

- Consider applying before October 2026. Banks will start adjusting risk models 6 to 12 months before April 2027 as they prepare internal systems. Getting sanctioned under current criteria is still possible if you move early.

- Don’t scatter-apply to multiple lenders. Every hard enquiry pulls your score down and signals credit hunger. Figure out which lender suits your profile first, then apply once.

- A larger down payment helps more than you think. Lower loan-to-value reduces the bank’s provisioning risk, which translates to better terms even at a borderline score.

How to choose the right home loan lender for your profile — Butter Money guide.

FAQs:

Q1.What is the RBI ECL framework?

The Expected Credit Loss framework requires banks to estimate future loan defaults in advance and hold funds against them — rather than waiting for loans to go bad. It takes effect April 1, 2027, and aligns Indian banking with global standards already in use across most of Asia, Europe, and the UK.

Q2.Does a CIBIL score below 730 mean my home loan gets rejected?

Not automatically. It means banks will likely price the higher risk into your interest rate or ask for more collateral. Some lenders will still approve loans below 730 — but typically at a higher rate that adds real money to your total repayment over 20 years.

Q3.What CIBIL score do I need for a home loan in 2027?

730 or above is where most banks are expected to offer standard terms. 750 and above typically gets the most competitive rates. Below 700, expect tighter scrutiny and higher rate premiums.

Q4.Will my existing home loan be affected?

No, if you’re paying on time. ECL doesn’t let banks change the terms of a currently performing loan. But if you miss payments after April 2027, banks may escalate your loan’s classification faster than they do today.

Q5.How quickly can I improve my CIBIL score? Six to nine months of consistent payments, reduced credit card utilization, and no new credit applications typically moves a score from the 650–700 range to above 730. The improvement is not instant but it is predictable.

Q6.What is Stage 2 provisioning and why does it matter for borrowers?

Stage 2 is when a bank sees elevated risk on a loan — usually 30 to 89 days overdue, or when early warning signals appear. Under the new rules, Stage 2 provisioning jumps from roughly 0.40% to a minimum of 5% of the loan amount. That 12x increase gives banks a strong financial reason to be more selective at the application stage, before loans get there.

Q7.Can I still get a home loan with a score below 730 after April 2027?

Yes, through some lenders. Housing finance companies and certain NBFCs may still approve loans below 730. The cost is usually a higher interest rate — 0.50% to 1% more. On a large loan over a long tenure, that adds up to several lakh rupees in extra interest.