Everything About Legal & Technical Verification in Home Loan

Everything About Legal & Technical Verification in Home Loan

Your salary slips are in. Your CIBIL is 780. The banker has all but shaken your hand. Then, a week later, the sanctioned amount lands ₹4–5 lakh lower than you planned — or the file just sits, “under process,” for two weeks.

Nine times out of ten, the reason is the same: legal and technical verification. It’s the stage where the lender stops checking you and starts checking the property. Two separate teams — one legal, one technical — decide whether the home you’ve picked is safe to lend against, and how much it’s really worth. Their reports can approve your loan, quietly shrink it, or stop it cold.

Here’s everything that happens at this stage, and how to come out of it with your loan intact.

Not sure what your profile and property can support? Check your eligibility with Butter Money in about two minutes — free, no branch visit, no impact on your credit score.

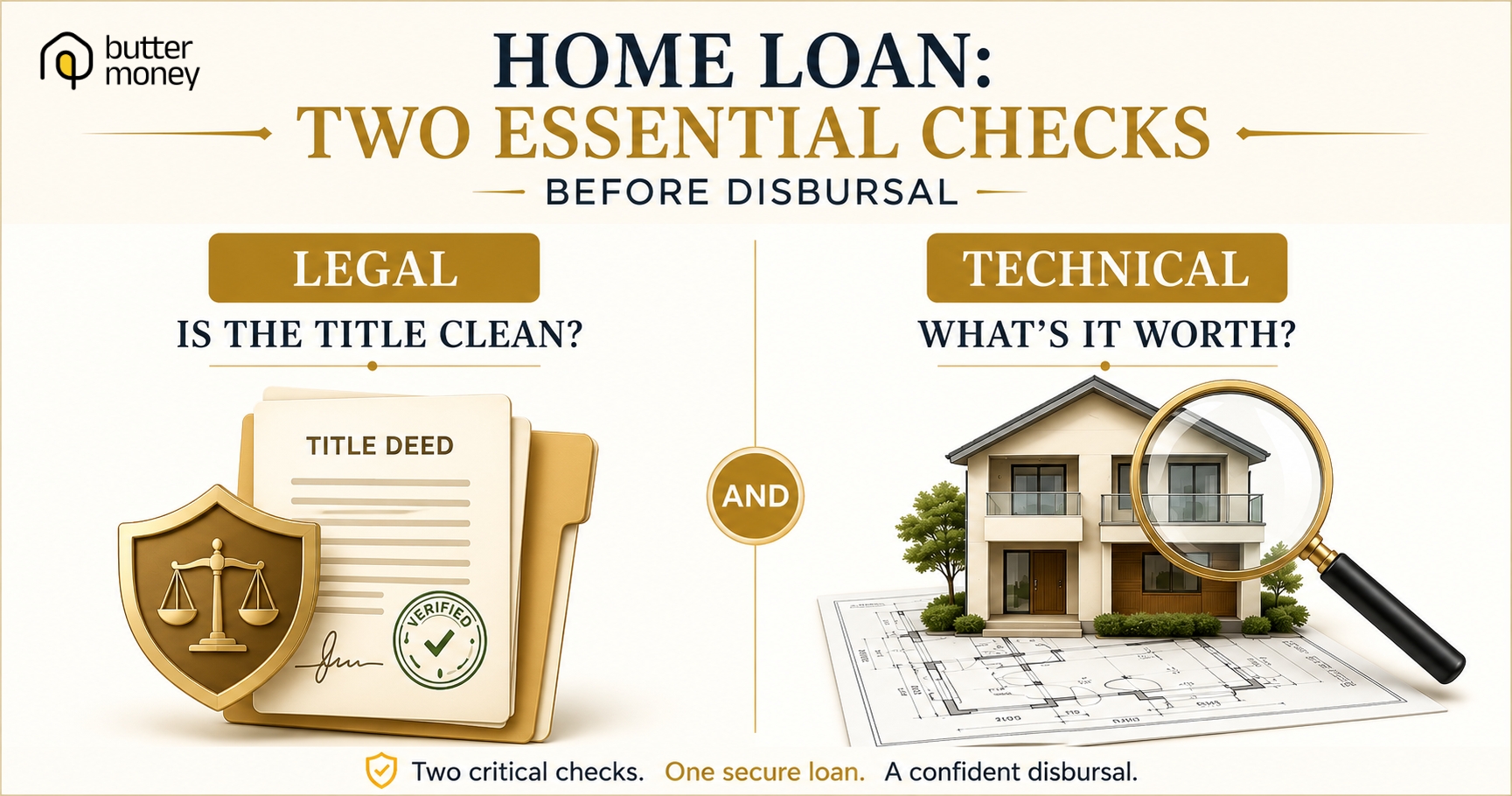

1. What it means

Legal and technical verification is a two-part check the lender runs on the property — not on you — before releasing the loan.

- Legal verification confirms the property’s ownership is clean, clear, and dispute-free.

- Technical verification — confirms what the property is genuinely worth today, and that it’s structurally sound and built to approvals.

Both produce a written report for the lender’s credit team. Only after both are clear does the loan move to final sanction and disbursal.

The key idea most explainers bury: income, employment, and CIBIL checks are about your ability to repay. These two checks are about the asset the bank will hold as security until your last EMI. A spotless personal profile can’t rescue a problem property.

2. Why it’s needed — and when it’s done

Why the lender does it:

- The property is the collateral. If you stop paying, the bank must be able to take and sell it without a court fight — so the title has to be clean.

- The loan amount is capped by what the property is actually worth, so the bank needs an independent valuation, not your negotiated price.

- It protects you too — it surfaces disputes, unapproved construction, or overpricing before you’re locked in for 20 years.

Why it matters to your wallet:

- A high income and credit score cannot override a shaky title or a low valuation.

- The outcome here directly sets your final loan amount and therefore your down payment.

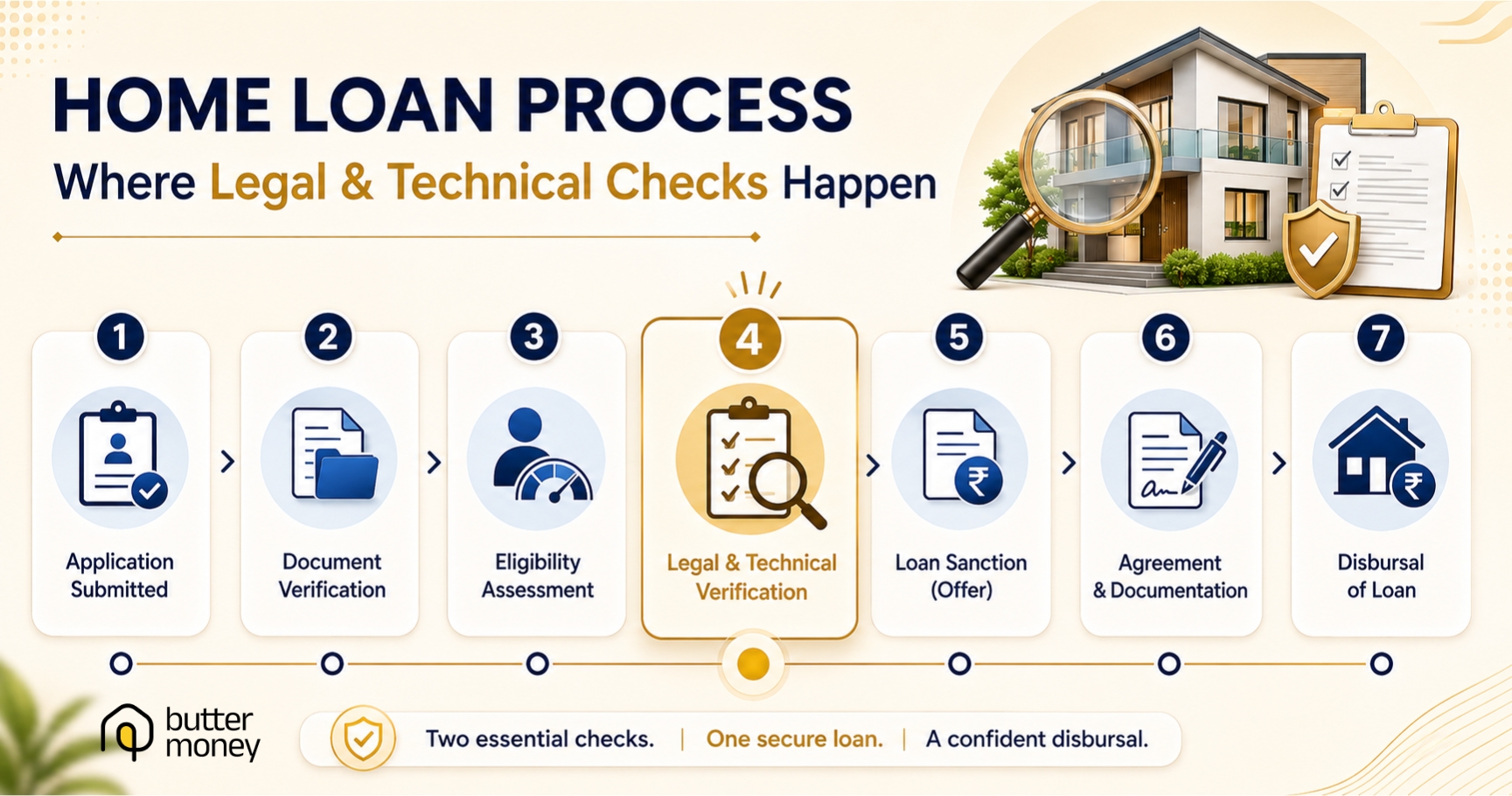

When it happens in the process:

- You apply and submit documents

- Profile + income + CIBIL checked

- Personal discussion

- → Legal & technical verification of the property (you are here)

- Final sanction

- Loan agreement + down payment

- Disbursal

3. How it’s done — process and checklist

Legal verification (two passes)

A panel lawyer examines the ownership trail.

Pass 1 — document scrutiny. The lawyer checks:

- Title/sale deed — proof that the seller genuinely owns the property

- Chain of title — the unbroken sequence of past owners (gaps here are a common stall)

- Encumbrance Certificate (EC) — that the property isn’t already mortgaged or disputed

- Approved building plan — that the structure matches what the authority sanctioned

- NOCs — from society, builder, or authority where applicable

- Property tax receipts — up to date, in the correct owner’s name

Pass 2 — the search. The lawyer independently checks the sub-registrar’s records to confirm your documents match the public record and no fresh lien or litigation has surfaced.

Output: a title report — clean, or “qualified” (flagged).

Technical verification (site visit)

An empanelled engineer or architect physically visits the property and assesses:

- Fair market value — an independent estimate of today’s worth

- Construction stage & quality — how much is built (for under-construction); structural condition (for ready homes)

- Approvals adherence — does what’s standing match the sanctioned plan? (extra floors, covered setbacks get flagged)

- Age & area — built-up/carpet area, and property age (roughly 25+ years can mean a lower loan share)

Output: a valuation report with the bank’s assessed value.

Your prep checklist (speeds this up)

- Complete, correct document set handed over on day one

- EC and latest property tax receipts in the current owner’s name

- Approved building plan/occupancy certificate available

- All applicable NOCs collected from the seller/builder

- Sale agreement conditions cover title fixes and dues clearance

4. Results and output

Both reports go to the credit team, and together they decide how much loan you actually get.

As per RBI guidelines, lenders sanction against the property’s fair market value assessed by an approved valuer — not the price you negotiated, and not the government circle rate. On top of that sit the RBI’s loan-to-value (LTV) caps:

| Property value | Maximum LTV | You fund at least |

| Up to ₹30 lakh | 90% | 10% |

| ₹30 lakh – ₹75 lakh | 80% | 20% |

| Above ₹75 lakh | 75% | 25% |

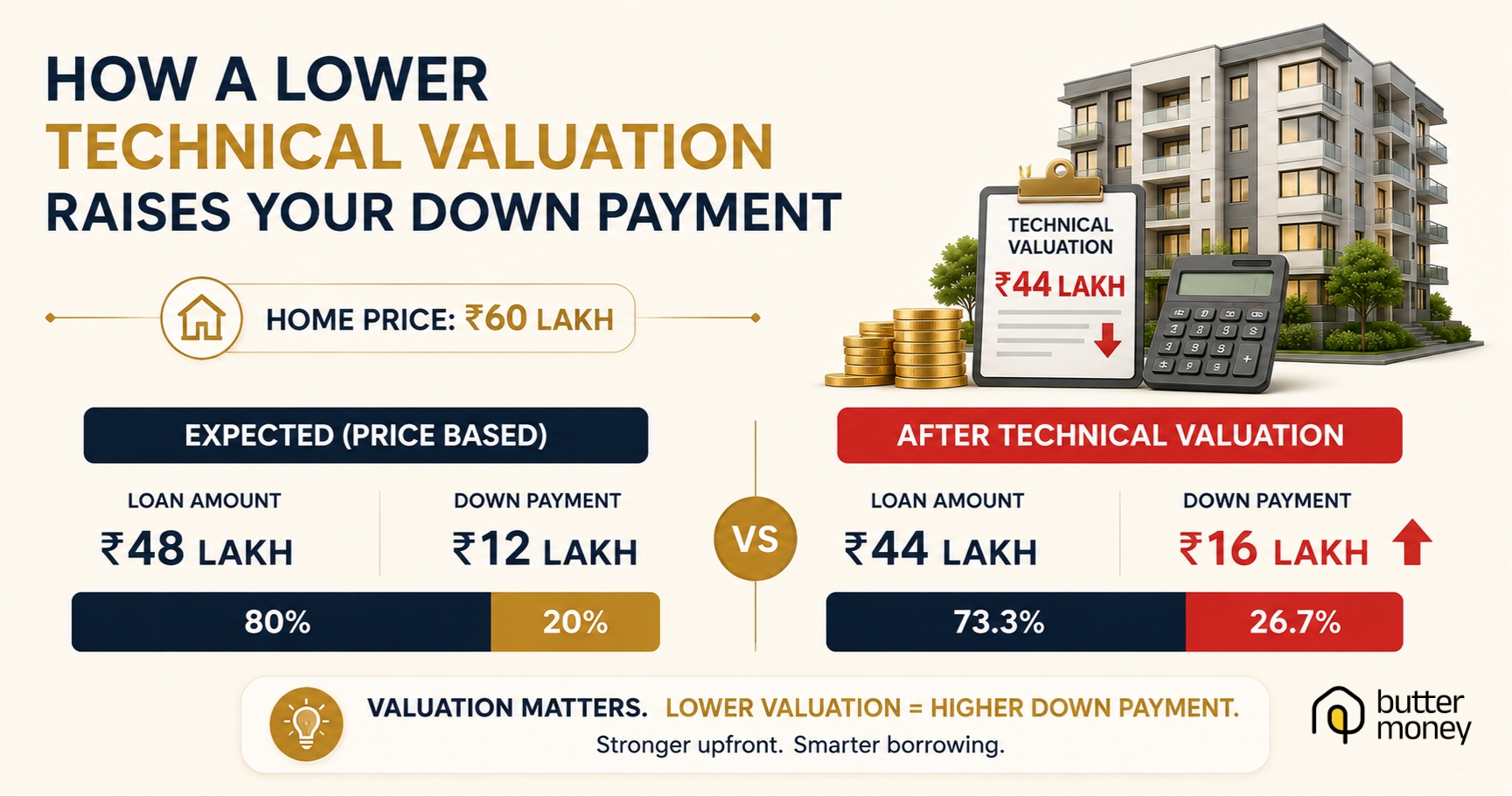

The catch: the loan is calculated on the lower of your agreed price or the bank’s valuation. A conservative valuation quietly raises your down payment.

Worked example — a Bengaluru-typical flat:

- Agreed price: ₹60 lakh → you expect 80% = ₹48 lakh loan, ₹12 lakh down

- Valuation comes in at ₹55 lakh (a normal, conservative read)

- Loan is now 80% of ₹55 lakh = ₹44 lakh

- Your gap to the ₹60 lakh price is now ₹16 lakh, not ₹12 lakh

A ₹5 lakh valuation gap just added ₹4 lakh to your down payment — and that’s before stamp duty and registration, which RBI rules keep out of the loan (you pay those separately, typically 3–8% of value depending on your state).

The one thing to internalise: the number that decides your loan isn’t the price you negotiated — it’s the valuer’s.

Want to see how a given loan amount changes your monthly EMI before you commit? Run it on Butter Money’s EMI calculator — instant, free, no sign-up to try.

Timeline & fees:

- Typically, 3–7 working days once the lender has all documents

- Incomplete papers or a complex title can stretch it to about two weeks

- Some lenders charge legal (~₹4,000–5,000) and technical (~₹3,000–5,000) separately (indicative); others fold them into the processing fee — check your sanction terms

5. Common outcomes — and what to do about them

Most stalls and cuts trace back to a short list. Here’s the move for each.

| What gets flagged | What to do |

| Valuation below the agreed price | Get the figure in writing; arrange the extra down payment, renegotiate with the seller using the valuation as leverage, or request a re-valuation with genuine comparable sales |

| Gap in the chain of title | Seller’s problem to fix — ask for the missing link deed/rectification; don’t pay beyond a refundable amount until the title report is clean |

| Deviated / unapproved construction | Get it regularised with the local authority, or treat it as a reason to walk — lenders rarely finance the unapproved portion |

| Missing NOC / occupancy certificate | Push the builder or society before disbursal; for a ready home, no OC is a serious flag, not a formality |

| Property tax dues in the seller’s name | Make clearing dues a written condition of sale |

The through-line: the moment a report is qualified, get the specific reason in writing and fix the document — not the paperwork around it.

When the report going against you is protecting you

An adverse finding feels like the bank sabotaging your purchase. Often it’s the opposite:

- A title dispute the legal search surfaces — annoying now, but if you’d paid in full without a loan, you’d have bought a property you might spend years litigating to own. The bank’s caution just saved you.

- A valuation well below asking price — often means the property is simply overpriced, and you were about to overpay with money you’d repay for two decades. That’s expensive information delivered early.

Two times to pause the purchase, not push the loan:

- A title defect the seller can’t cleanly fix

- A valuation gap so large it signals you’re overpaying, not that the valuer was harsh

A property that clears both checks is one you can buy with confidence. Check your eligibility with Butter Money to see what a verified property unlocks for your profile — free, no credit-score impact.

6. How Butter Money helps

Butter Money is built to keep this stage from becoming the place your loan mysteriously shrinks:

- Eligibility clarity up front — see a realistic loan range for your profile before you fall for a property, so a low valuation doesn’t blindside your budget

- Document guidance — a clear checklist of exactly what the legal and technical teams will want, so you hand over a complete set on day one and don’t lose a week to missing papers

- Straight answers on outcomes — if a valuation comes in low or a title is flagged, you get the plain-English reason and your options, not a vague “under process”

- No inflated promises — you’ll get a grounded read on what your property and profile actually support

Go in knowing the valuer’s number matters more than the sticker price, keep your documents complete, and treat a clean title report as the real green light. Do that, and this stage stops being a mystery — it becomes the moment a good purchase gets confirmed. Homeownership is well within reach; it’s just worth reaching for the right property.

Ready to start on solid ground? Check your home loan eligibility with Butter Money — free, in minutes, with no impact on your credit score.

7. FAQs

What is legal and technical verification in a home loan? A two-part check the lender runs on the property before disbursal. Legal verification confirms the title is clear and dispute-free; technical verification assesses fair market value, construction quality, and adherence to approvals. Both must be cleared before the final sanction.

Can my home loan be rejected even if my income and CIBIL are fine? Yes. These checks run on the property, not on you. A title gap, unapproved construction, or a low valuation can reduce or reject the loan regardless of how strong your personal profile is.

Why did the bank sanction less than I expected? Usually, because the technical valuation came in below your agreed price. The loan is calculated on the lower of your price or the bank’s valuation, and RBI’s LTV caps apply to that figure — so a conservative valuation raises your down payment.

How long does legal and technical verification take? Typically 3–7 working days once the lender has all documents. Missing papers or a complex title can extend it to about two weeks.

Who pays for legal and technical verification? The borrower. Some lenders charge legal and technical fees separately; others include them in the processing fee. Check your sanction terms.

What documents does the legal team check? Title/sale deed, chain of title, Encumbrance Certificate, approved building plan, applicable NOCs, and property tax receipts — cross-verified against the sub-registrar’s records.

Can I challenge a low property valuation? You can request a re-valuation if you have genuine comparable sales, arrange the higher down payment, or use the valuation to renegotiate the price with the seller.