No Credit History? How to Get Your First Home Loan in India

You earn well. You save every month. Your rent has never been late. But when you check your CIBIL report, it says “NH” or shows a score of -1, and suddenly you are not sure any bank will lend you the money for your first home.

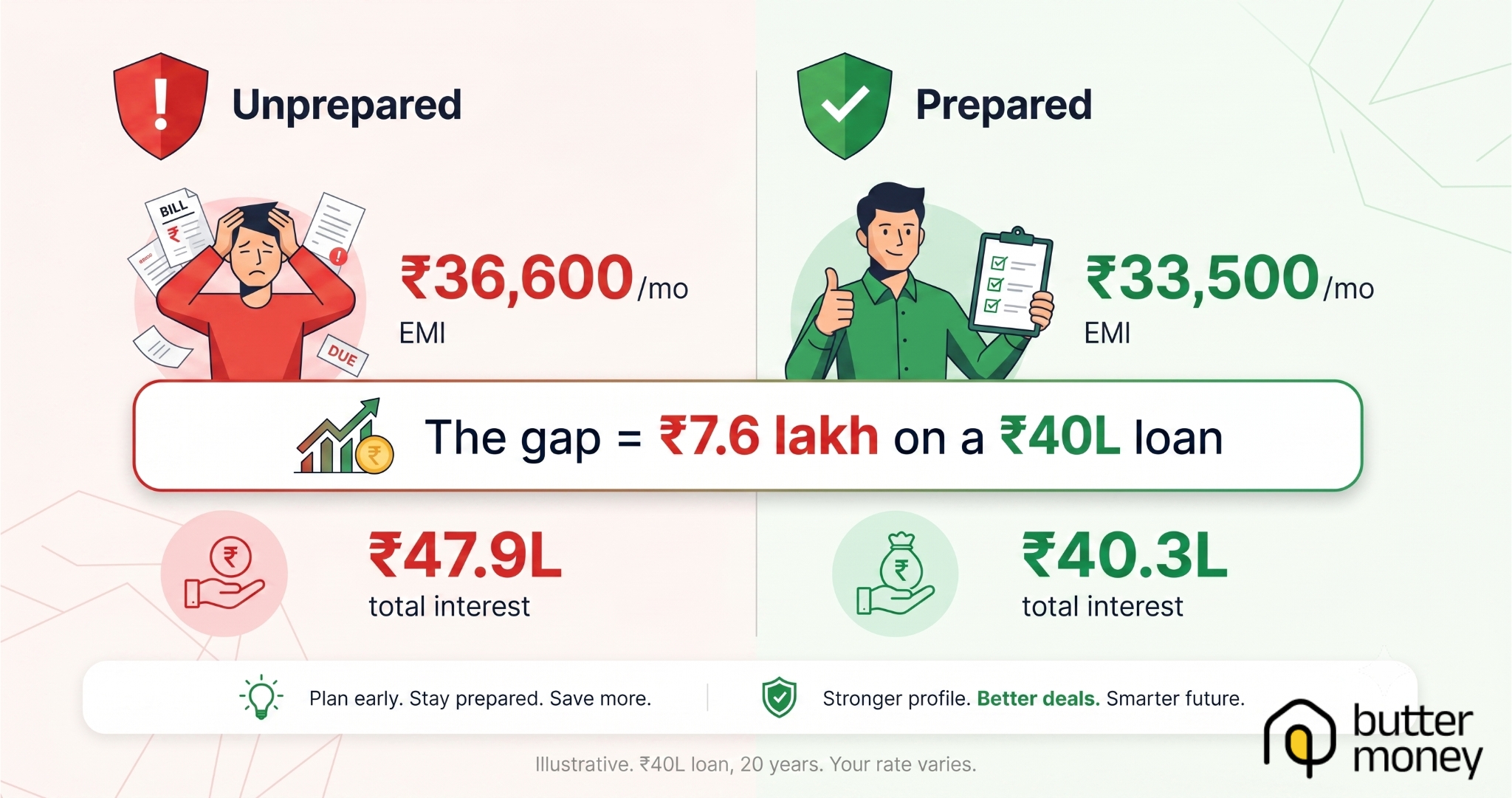

Here is the part most articles skip: with no credit history, the real risk is rarely rejection. If your income is steady, a lender will usually approve you. The risk is the rate they charge while they figure out whether to trust you. On a ₹40 lakh loan, walking in unprepared instead of prepared can cost you around ₹3,000 more every month and roughly ₹7.5 lakh more over 20 years. That gap is the whole reason this guide exists.

This article shows you exactly what lenders look at when you have no score, what documents to keep ready, which lenders are friendlier to first-timers, and how to avoid the small mistakes that quietly push your rate up.

Not sure where you stand? Check your home loan eligibility in 2 minutes with Butter Money. It is free, runs entirely online, and does not touch your CIBIL score.

Can you actually get a home loan with no credit history?

Yes. Having no credit history is not the same as having a bad one, and lenders treat the two very differently.

A blank file means the bureau simply has no borrowing record to score. According to TransUnion CIBIL, a profile with no past loans or credit cards shows up as “NH” (no history) or a score of -1, while a profile with less than six months of activity may show “NA” or 0. A low score, on the other hand, signals missed payments or defaults. In a lender’s eyes, NH is a clean slate. A score of 580 is a warning sign. You are starting from the better of the two positions.

What this means in practice: a no-score borrower with proof of stable income is far more lendable than a borrower with a damaged score. Your job is not to “fix” your CIBIL before you apply. Your job is to give the lender enough evidence, through income and documents, that they do not need a score to feel safe.

NH, NA, -1: what each one means

- NH / -1: No credit history at all. You have never taken a loan or used a credit card.

- NA / 0: Some activity exists, but less than six months, so there is not enough data to generate a number.

- A real score (300 to 900): Built from at least six months of credit behaviour.

None of these block a home loan on their own. They just change how much weight the lender puts on the rest of your file.

What “no credit history” really costs you

This is the number to anchor on before anything else.

When a lender cannot read your repayment behaviour from a score, they price in some uncertainty. Walk in with a thin file and a weak application, and you land at the higher end of their range. Walk in prepared, with strong income proof and a healthy down payment, and you push toward the better end. The difference is not small.

A conservative example. Take a ₹40 lakh home loan over 20 years:

| Applicant | Indicative rate | Monthly EMI | Total interest paid |

| Rushed, thin file | ~9.25% | ~₹36,600 | ~₹47.9 lakh |

| Prepared, strong income proof | ~8.00% | ~₹33,500 | ~₹40.3 lakh |

| Difference | 1.25% | ~₹3,100/month | ~₹7.6 lakh |

These rates are illustrative, not quotes, and your actual rate depends on the lender, your income, and the loan size. But the shape of the gap is real: a 1% to 1.5% difference on a long-tenure loan compounds into lakhs. As of June 2026, the most competitive home loan rates in India start around 7.10% to 7.25% from public sector banks, but those are reserved for borrowers with a 750-plus score and a strong profile. A new-to-credit borrower will usually sit a notch above that floor, which is exactly why preparation pays.

See your own numbers, not an average. Run your loan amount and tenure through the Butter Money EMI calculator to see what a half-percent swing does to your total cost.

What lenders look at when there’s no score

With the score column blank, a lender leans harder on five things. Think of these as the file you are actually building.

1. Income stability. Steady, provable income is the single strongest signal. Salaried applicants with a few years at one employer, or a regular salary credit, score well here. Self-employed applicants need clean ITRs and consistent business inflows.

2. Employment quality. Working at a large, stable, or government organisation works in your favour. Lenders read it as lower risk of sudden income loss. Longer tenure at the same job helps more than a higher salary at a new one.

3. Down payment (your loan-to-value ratio). The more you put down, the less the lender risks. As per RBI’s loan-to-value guidelines, banks can typically fund up to 90% of property value on smaller loans, but for a no-score borrower, putting down 20% or more instead of the bare minimum is one of the fastest ways to win a better rate.

4. Banking behaviour. Your savings account tells a story even when your credit file does not. Regular balances, no bounced auto-debits, and steady inflows show financial discipline. Many newer lenders now read this directly as “alternative” credit data.

5. A co-applicant. Adding a co-applicant with an established score, often a spouse or parent, can lift both your eligibility and your rate. Their history fills the gap yours cannot.

If three or four of these are strong, your blank score stops mattering very much. That is the reframe: you are not asking the lender to overlook a weakness. You are handing them five other ways to say yes.

Want to know which of these five is your strongest card? A Butter Money advisor can read your profile and tell you where you stand before you formally apply. Talk to an advisor, no obligation.

Documents you’ll need

Keep these ready before you apply. A complete file moves faster and signals seriousness.

For everyone:

- PAN card and Aadhaar

- Recent passport-size photographs

- Property documents (agreement to sell, builder details, title papers)

If you are salaried:

- Last 3 months’ salary slips

- Last 6 months’ bank statements (the salary account)

- Form 16 or latest ITR

- Employment proof or offer letter

If you are self-employed:

- Last 2 to 3 years’ ITRs with computation

- Last 12 months’ bank statements (business and personal)

- Business proof (GST registration, shop licence, or similar)

- Profit and loss statement, ideally CA-certified

For a no-score borrower, the bank statements and ITRs do the heavy lifting. They are the substitute for the repayment history you do not yet have, so make sure they are clean and consistent.

Your step-by-step path to approval

A clear sequence keeps you from the mistakes that quietly raise your rate.

- Pull your own credit report first. Checking it yourself is a soft enquiry and does not affect anything. Confirm whether you show NH, NA, or a partial score, and check for errors.

- Fix your down payment. Decide how much you can put down. Aiming for 20% or more strengthens every part of your application.

- Use an eligibility checker before applying anywhere. This tells you your likely loan amount without creating a hard enquiry on your file.

- Shortlist the right lenders. Pick lenders that assess income and alternative data, not just the score (more on this below).

- Apply to one or two, not five. Every formal application is a hard enquiry. A burst of them across many banks signals “credit hunger” and can work against you.

- Submit a complete file. Missing documents stall approvals and invite tougher terms. Hand over everything at once.

Which lenders are friendlier to new-to-credit borrowers

Not all lenders treat a blank file the same way.

- Public sector banks (such as SBI, PNB, Bank of Baroda) offer the lowest rates but tend to weigh the score heavily. With no score, expect more documentation scrutiny, though strong income still gets you through.

- Private banks (such as HDFC, ICICI, Axis) often process faster and may look more holistically at income and employment, sometimes at a slightly higher rate.

- Housing finance companies and newer digital lenders are usually the most flexible on credit history. Many use alternative credit assessment, reading your banking behaviour and income directly. The trade-off is that their rates can run higher than a bank’s, so compare the total cost, not just the approval odds.

There is no single “best” lender for everyone. The right choice depends on whether your priority is the lowest rate (lean towards banks, and be ready to prove income) or the highest certainty of approval (a flexible HFC or digital lender may suit you, at a cost). This is where Butter Money helps: instead of applying blind, you can compare what different lenders would actually offer your profile, then choose on real numbers.

How long does it take?

For a well-prepared file, expect roughly:

- Eligibility check: a few minutes online

- Sanction (in-principle approval): 2 to 7 working days once documents are in

- Final disbursement: another 1 to 3 weeks, mostly tied to property and legal verification

A no-score profile can add a few days of extra scrutiny, but a complete document file is the single biggest lever on speed. Incomplete applications, not the missing score, cause most delays.

When you should wait (and build a thin file first)

Sometimes the smart move is to slow down. Applying now is not always the cheaper option.

Consider waiting a few months if:

- Your income is new or irregular. If you have been at your job or business for under a year, a few more months of steady salary credits or ITRs will materially improve your terms.

- You can only manage a very small down payment. Stretching to put down less than 10% pushes your rate up and your buffer down. Saving a little longer often costs less than the rate premium.

- You are tempted to take a loan just to “build credit.” This is the most common and most expensive mistake. Taking an unnecessary personal loan at 12% to manufacture a score can cost more than the home loan premium you are trying to avoid.

If you do want to build a thin file before a big loan, the gentle path is a secured credit card or a small, genuinely needed EMI purchase, repaid in full and on time for six months. That can move you from NH to a usable score without taking on costly debt. Waiting is not failure. For some profiles, six patient months turns a 9.25% offer into an 8% one, and that is real money.

Not sure whether to apply now or wait? A short conversation can save you lakhs. Get a free profile review from a Butter Money advisor and decide with the numbers in front of you.

The bottom line

A blank credit history feels like a locked door, but it is closer to an unwritten page. Lenders are not looking for a reason to reject you. They are looking for evidence that you will repay, and your income, your down payment, and your banking record are all evidence you already have. First-time buyers with no score get home loans in India every single day. The ones who get the best rate are simply the ones who walked in prepared. You can be one of them.

Start where it costs you nothing. Check your eligibility with Butter Money in 2 minutes, free, online, and with no impact on your CIBIL score.

Frequently asked questions

Q1.Can I get a home loan with no CIBIL score? Yes. A no-score profile (NH or -1) is not the same as a bad score. If your income is stable and provable, lenders will usually approve you based on income, employment, down payment, and banking behaviour instead of a score.

Q2.Will I pay a higher interest rate with no credit history? Often, slightly. A new-to-credit borrower usually sits a notch above the lowest advertised rates. A strong down payment, solid income proof, or a co-applicant with a good score can narrow or close that gap.

Q3.Does checking my own credit report hurt my score? No. Checking your own report is a soft enquiry and has no effect. Only a lender’s hard enquiry during a formal application can have a small, temporary impact.

Q4.Should I take a personal loan to build credit before my home loan? Usually no. An unnecessary loan taken only to build a score can cost more in interest than the home loan premium you are trying to avoid. A secured credit card or a small needed purchase, repaid on time, is the cheaper way to build a thin file.

Q5.How much down payment do I need with no credit history? Lenders can fund up to about 90% of property value, but with no score, putting down 20% or more strengthens your application and helps secure a better rate.

Q6.Which lenders are best for first-time buyers with no credit history? Housing finance companies and newer digital lenders tend to be the most flexible because many use alternative credit assessment. Banks offer lower rates but weigh income proof more heavily when there is no score.

Q7.How long does approval take? With a complete document file, sanction typically takes 2 to 7 working days and disbursement another 1 to 3 weeks. A missing score adds little time; incomplete documents add the most.