Bank vs HFC vs NBFC for Home Loan in India (2026): Which Lender Should You Choose?

Why Does it Matter Which Lender Category You Apply with Before the Rate?

The problem that most home loan applicants fall into is that they chase the lowest headline interest rate without understanding which lender category actually fits their profile.

And what happens because of this mistake?

1. A rejected application hurts your CIBIL score. Every formal home loan application triggers a hard inquiry on your credit report, visible to all future lenders for 24 months. A single hard inquiry can drop your CIBIL score by 5–10 points. Apply to three lenders in two months, and your fourth lender will see a borrower who has already been declined or quoted unfavourably elsewhere. They price that risk into your offer.

2. The wrong lender means months of wasted time. Banks can take 2–4 weeks to reject an application that an experienced advisor could have predicted upfront. That delay can cost you a property deal.

Before applying anywhere, check your home loan eligibility with zero CIBIL impact. Butter Money’s ++Eligibility Check++ matches your profile to the right lender across 30+ institutions, with no hard inquiry and no score drop.

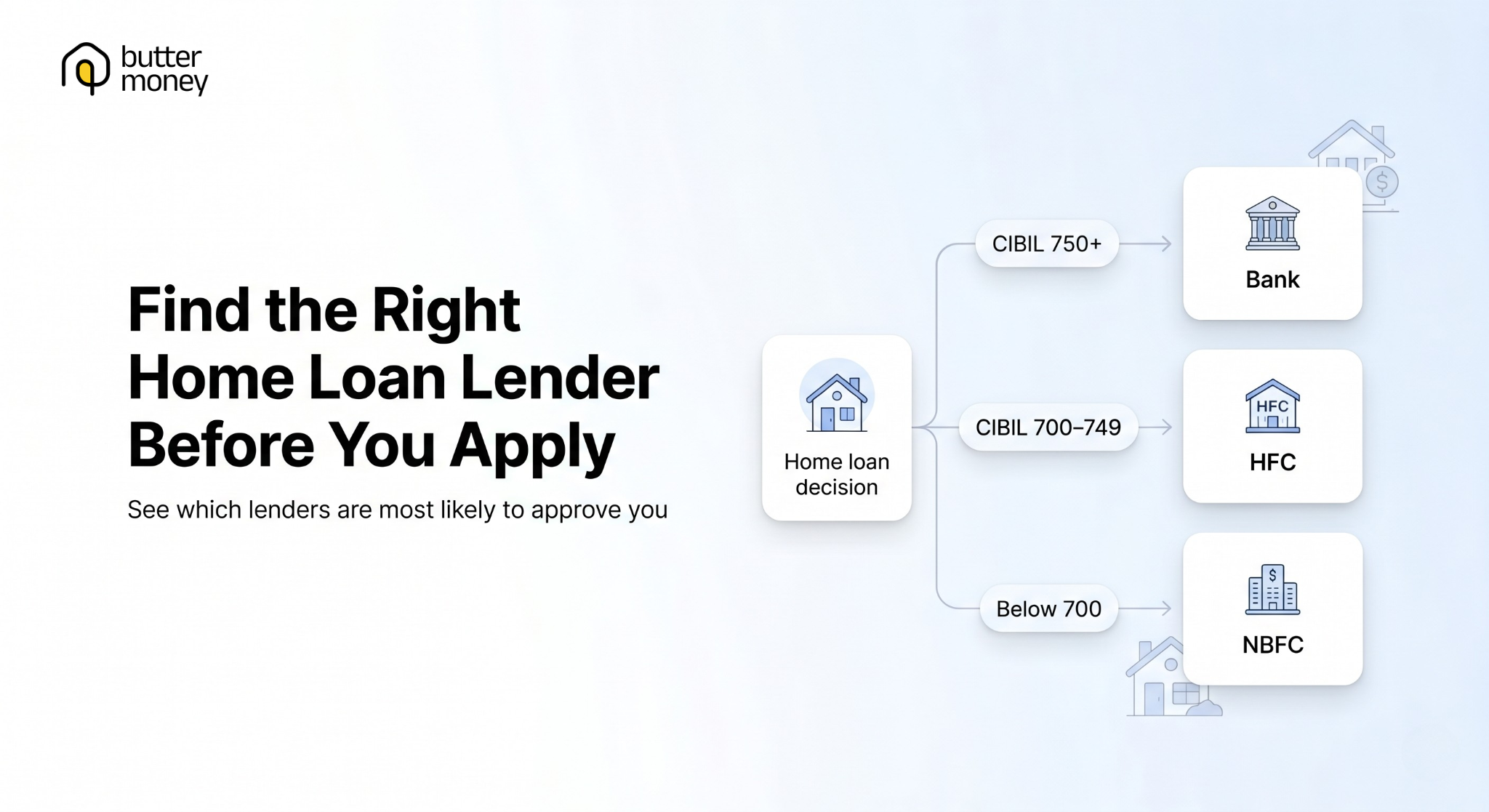

Understanding the three lender categories is the most important step you can take before you apply.

What Are Banks, NBFCs, and HFCs?

Banks: The Lowest-Rate Default

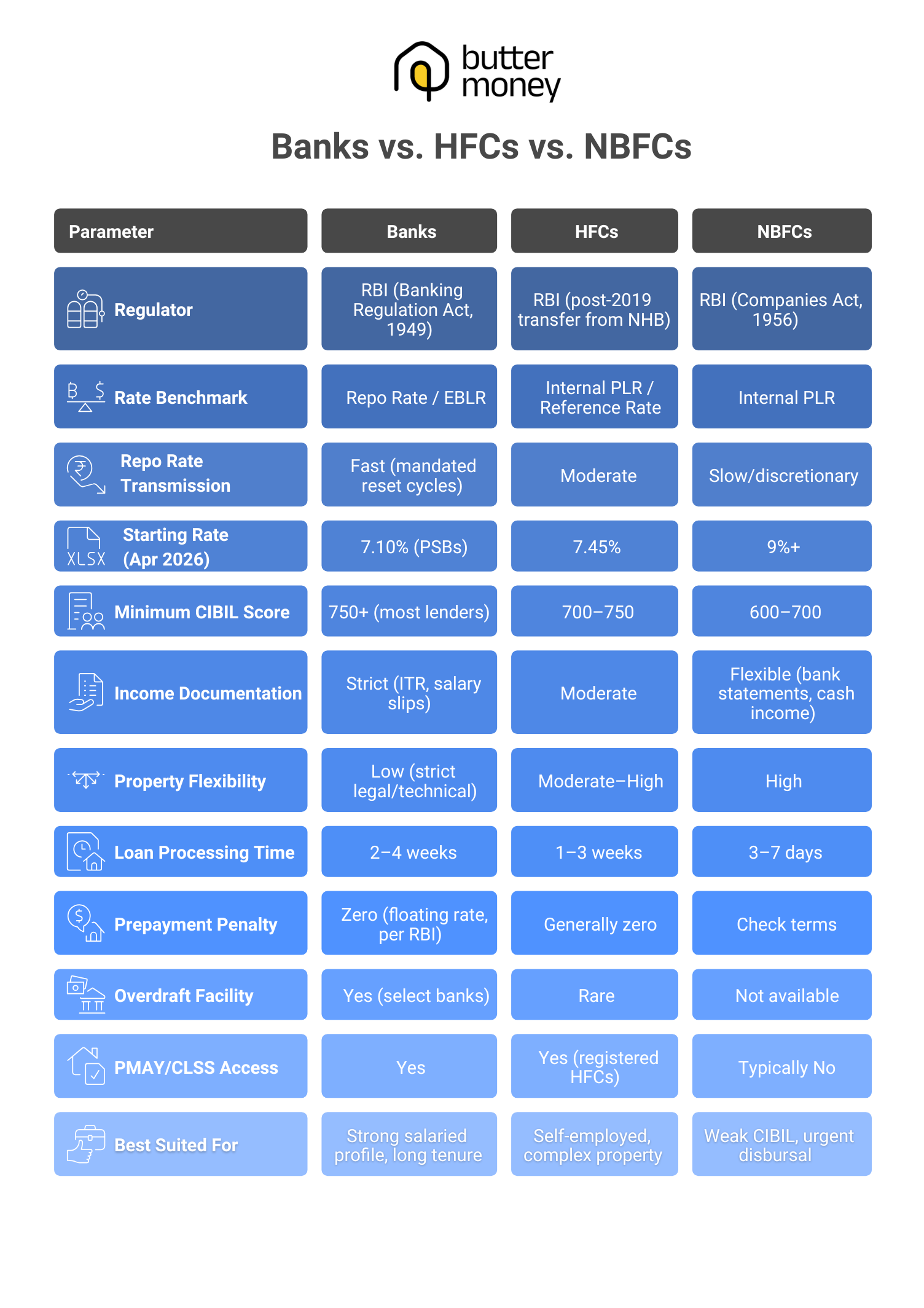

Banks operate under the Banking Regulation Act, 1949, and are directly regulated by the Reserve Bank of India (RBI). Only banks are allowed to collect CASA (Current and Savings Account) deposits from the general public.

How does this impact housing loans? Banks have a very low cost of raising funds through borrowing from depositors at 3%-4% interest (savings account interest rate), thereby being the lowest among all other categories of lenders. These costs are reflected in some of the best home loan interest rates offered by banks in India.

From October 2019 onwards, all newly originated floating-rate home loans offered by banks need to be benchmarked against the External Benchmark Lending Rate (EBLR), which is mostly the RBI Repo Rate, currently pegged at 5.25%, as on April 2026 (unchanged by the MPC at its meeting on April 8, 2026, after reducing it by 125 bps cumulatively in 2025). With this system in place, rate reduction gets immediately reflected in reduced EMIs on home loans with automatic recalibration.

Banks also offer two unique features:

- No prepayment penalty on floating rate home loans for individuals (as per RBI guidelines)

- Overdraft or Max Saver facility: Your home loan balance is connected to your savings account. Each extra rupee kept in this account helps reduce the loan balance subject to interest charges – potentially saving lakhs over a long repayment period.

See exactly how much an overdraft home loan can save you using Butter Money’s ++Overdraft Calculator++.

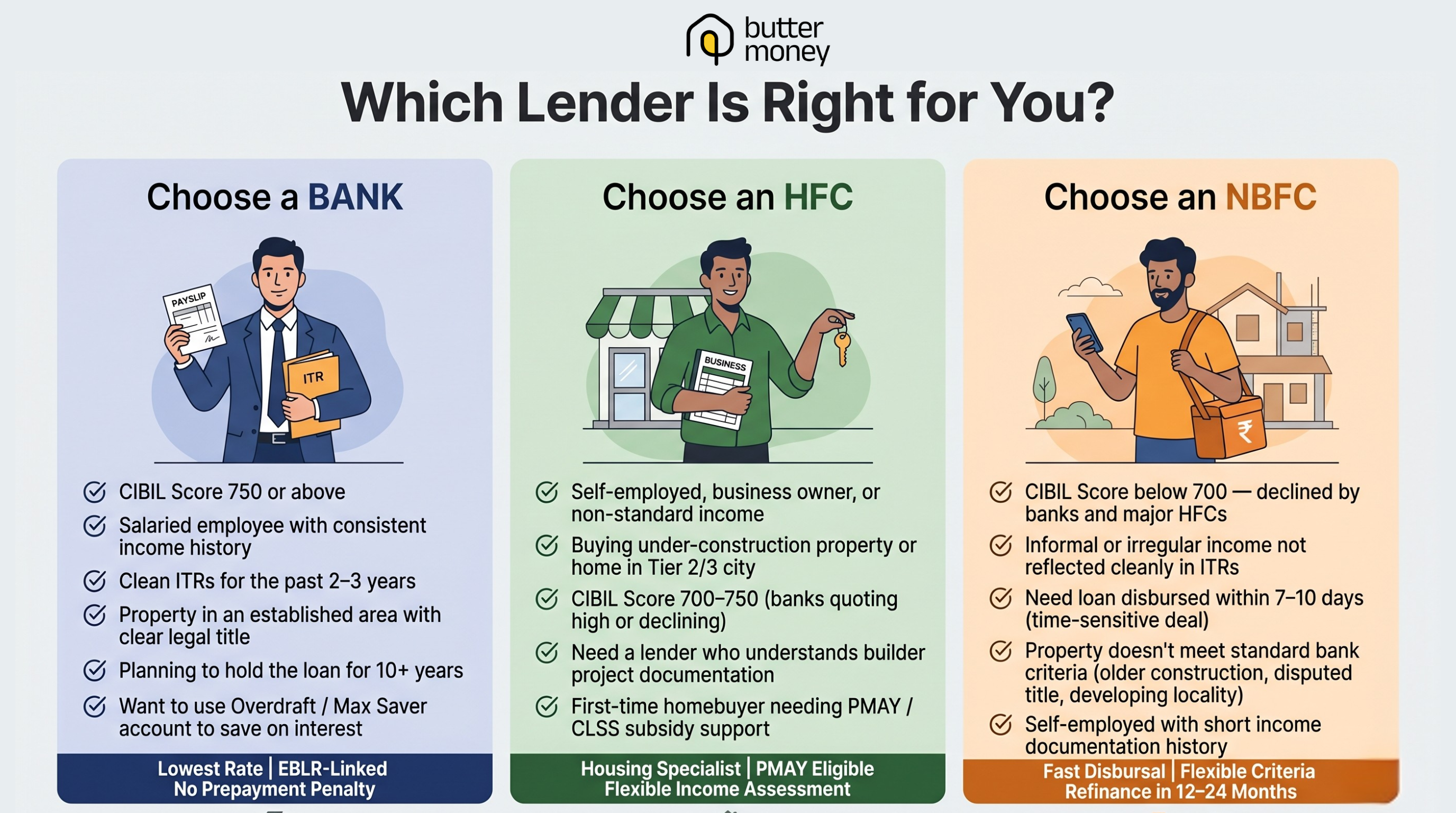

The Bank Catch: Banks are conservative and paperwork-intensive. Most need a CIBIL score of 750+ and clear ITRs for 2-3 years, along with complete legal and technical clearance of the property. If your property has any deviations from the sanctioned building plans or your salary is inconsistent, most banks will refuse.

Related: ++Why Your Home Loan EMI Didn’t Drop After the RBI Rate Cut — MCLR vs EBLR Explained (2026)++

NBFCs: The Speed-and-Flexibility Lenders

Non-Banking Financial Companies (NBFCs) are registered entities under the Companies Act, 1956 and supervised by RBI, although under a more relaxed regime compared to banks. Demand deposits and a banking license are not within their scope.

In the home loan industry, NBFCs fill the gaps that banks and HFCs won’t touch:

- Borrowers with CIBIL scores less than 700

- Self-employed individuals, gig workers, and informal income earners

- Developing real estate with complicated or missing title deeds

- Smaller loan amounts in the ₹10–30 lakh range for affordable housing

Interest Rate structure: The home loan interest rates by NBFCs are determined based on their internal Prime Lending Rate (PLR), not the RBI repo rate. They have more flexibility to change interest rates, and this could lead to a delay in the transmission of interest cuts from the central bank. Interest rates offered by NBFCs for home loans range between 9% to 14%.

Where NBFCs genuinely excel:

- Processing speed: Many non-bank financial institutions offer loan sanctions and disbursal in just 3 to 7 working days, which can be vital in negotiating a timely property purchase

- Flexible income assessment: NBFCs examine your repayment capacity based on bank statements, cash flow, and other factors like income from cash transactions instead of ITR

- Lower CIBIL threshold: NBFCs generally accept loan applications with CIBIL scores ranging between 600 and 740, which would be rejected by traditional banks

Your CIBIL score is low, but you want a home loan now? Don’t get stuck. Read: ++How to Get a Home Loan With a Low CIBIL Score++

Important: The NBFC home loan is usually just the beginning, not the end. After building a good track record for 12 to 24 months of timely payments, one could then consider a balance transfer to a bank or HFC at reduced interest rates.

Calculate exactly how much a balance transfer saves you using Butter Money’s ++Balance Transfer Calculator++.

Housing Finance Companies (HFCs): The Housing Specialists

HFCs are a legally defined subcategory of NBFCs. By RBI definition, an entity qualifies as an HFC if:

- At least 60% of its total financial assets should consist of housing finance, AND

- At least 50% of those should comprise home loans to individuals

Regulation: HFCs were initially regulated by the National Housing Bank (NHB). However, since 2019, HFCs have been subject to the same RBI regulations as banks, except with certain operating differences.

How HFCs fund home loans: While HFCs do not have demand deposits as a funding source like banks, they raise funds through lines from NHB, issuance of bonds/debentures, and borrowings from banks, thus having relatively higher costs of funds

Rate benchmark: HFCs price loans against an internal Prime Lending Rate (PLR) or interest rate, not the repo rate. This implies that rate cuts initiated by the RBI do not automatically apply to HFCs, but most major HFCs in India have been passing on most rate cuts from 2025 voluntarily.

Major HFCs in India (2026):

| HFC | Starting Rate (p.a.) |

|---|---|

| LIC Housing Finance (LIC HFL) | 7.50%+ |

| Bajaj Housing Finance | 7.45%+ |

| ICICI Home Finance | 7.50%+ |

| PNB Housing Finance | 8.50%+ |

| Tata Capital Housing Finance | 7.75%+ |

| Aditya Birla Housing Finance | 8.25%+ |

| Aadhar Housing Finance | 11.75%+ |

Source: Business Standard / Paisabazaar, April 2026. Rates subject to borrower profile.

Why HFCs often beat banks for non-standard profiles:

- More willing to lend on under-construction projects, resale properties, and properties in semi-urban or Tier 2/3 cities

- More flexible with self-employed borrowers and mixed income documentation

- Some major HFCs — like LIC HFL and Bajaj Housing Finance — offer starting rates that rival leading private banks

- Most are registered Central Nodal Agencies for PMAY-CLSS (Credit-Linked Subsidy Scheme), so eligible first-time buyers can access government subsidies through them

Are you self-employed and unsure which lender will approve you? Read: ++Home Loan for Self-Employed in India: Eligibility, Documents & Approval Tips (2026)++

Home Loan Interest Rates: Banks vs HFCs vs NBFCs (April 2026)

RBI Repo Rate stands at 5.25% as on April 8, 2026 (unchanged since the last Monetary Policy Committee meeting). In 2025, the RBI cut the repo rate by a total of 125 basis points, drastically reducing the minimum for bank housing loans.

Bank Home Loan Interest Rates (April 2026)

| Lender | Starting Rate (p.a.) | Rate Range (p.a.) |

|---|---|---|

| Public Sector Banks | 7.10% | 7.10%–9.50% |

| State Bank of India (SBI) | 7.50% | 7.50%–8.70% |

| Canara Bank | 7.10% | 7.10%–9.00% |

| Bank of Maharashtra | 7.10% | 7.10%–9.00% |

| Private Sector Banks | 7.65% | 7.65%–12.58% |

| ICICI Bank | 7.65% | 7.65%–9.65% |

| Kotak Mahindra Bank | 7.70% | 7.70%–9.10% |

| HDFC Bank | 7.75% | 7.75%–10.05% |

| Axis Bank | 8.35% | 8.35%–11.90% |

Source: Paisabazaar, BankBazaar, Upstox — April 2026. Rates are indicative; the final rate depends on CIBIL score, income, and loan amount.

HFC Home Loan Interest Rates (April 2026)

| HFC | Starting Rate (p.a.) |

|---|---|

| LIC Housing Finance Limited | 7.50% |

| Bajaj Housing Finance Limited | 7.45% |

| ICICI Home Finance Company Limited | 7.50% |

| Tata Capital Housing Finance Limited | 7.75% |

| PNB Housing Finance Limited | 8.50% |

| Aditya Birla Housing Finance Ltd (ABHFL) | 8.25% |

| Aadhar Housing Finance Limited | 11.75% |

Source: Business Standard, Tata Capital, BankBazaar — April 2026.

NBFC Home Loan Interest Rates (April 2026)

General NBFCs (not specialist housing companies) usually charge home loans at an interest rate of 9% – 14%+ p.a., based on the borrower’s profile.

Use Butter Money’s ++EMI Calculator++ to see how even a 0.5% rate difference changes your total interest outgo across a 20-year tenure. On a ₹50 lakh loan, that difference can exceed ₹3–4 lakhs.

Key Differences: Full Comparison Table

Related Read: ++RBI’s No Foreclosure Penalty Guideline 2026: What Every Home Loan Borrower Must Do This Month++

HFC vs NBFC: What’s the Difference?

When exploring home loan options in India, you may come across Housing Finance Companies (HFCs) and Non-Banking Financial Companies (NBFCs). While both are RBI-regulated non-bank lenders, they differ mainly in their purpose and scope.

Housing Finance Company (HFC)

- A housing finance company focuses primarily on home loans and housing-related finance, such as property purchase, construction, or renovation.

- Earlier regulated by NHB, HFCs are now regulated by RBI (since 2019).

- Their lending processes are usually designed specifically for housing finance and property-related borrowers.

Non-Banking Financial Company (NBFC)

- A non-banking financial company is a broader category of financial institution that provides multiple types of credit.

- NBFCs offer various loans, including personal loans, business loans, vehicle loans, and sometimes NBFC home loans.

- There are multiple types of NBFCs in India, each focusing on different lending segments.

In simple terms:

All HFCs are specialized housing lenders, while NBFCs are broader financial institutions that may or may not focus on home loans.

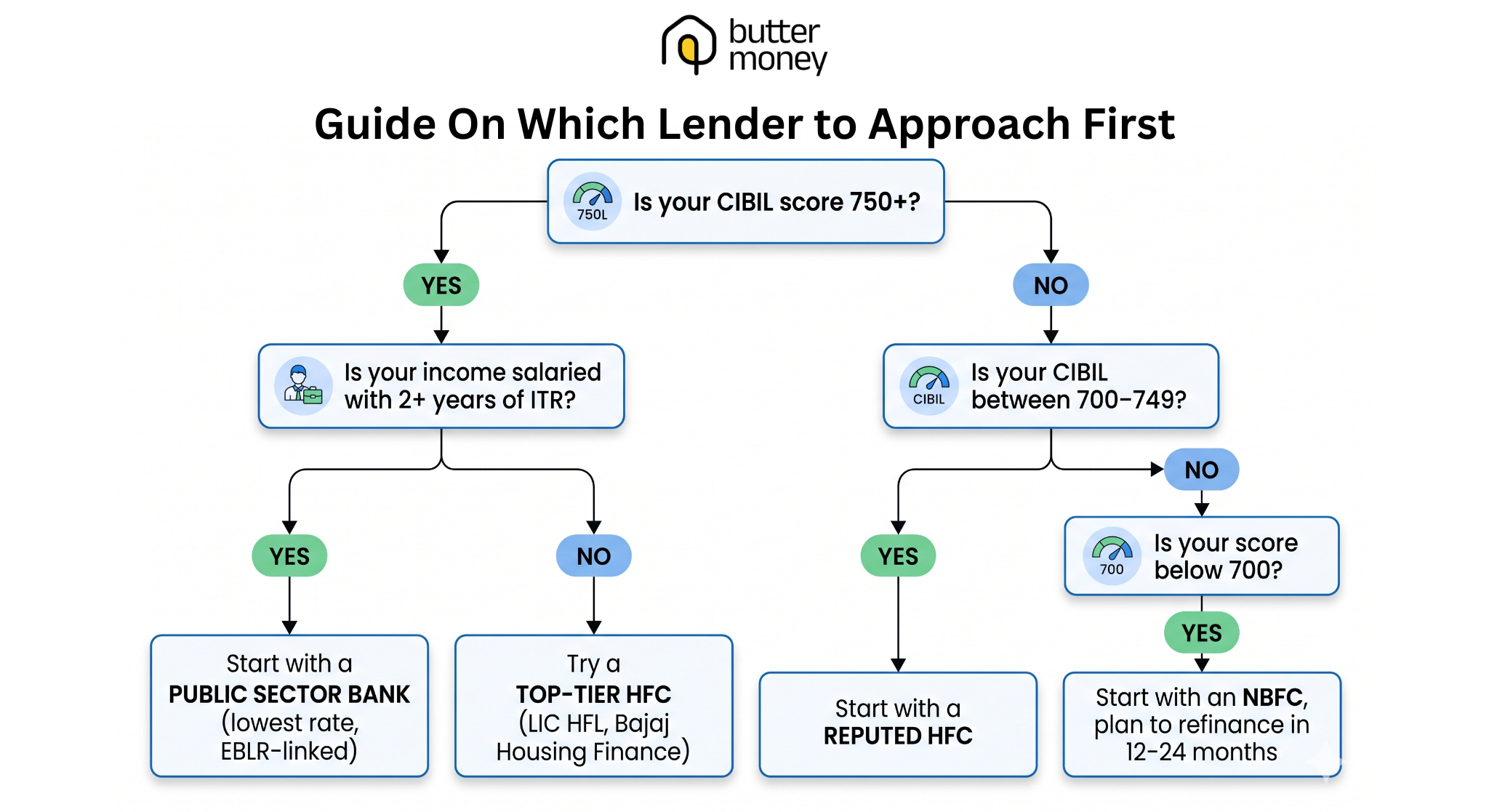

Which Lender Type Actually Suits?

Thinking about applying together with your spouse or parent to increase eligibility? Read: ++Buying a Home Together? What You Need to Know Before Signing a Joint Home Loan++

The CIBIL Score Risk: Why Sequence Matters

Here is a scenario that plays out every day in India:

A borrower applied at SBI, but was declined (CIBIL score is 735, slightly below their cut-off). Applied at ICICI Bank, offered 9.25%; too much. Applied at PNB Housing Finance, approved at 8.90%. Now, three hard inquiries in just two months.

The next lender, or any future lender, now sees a borrower who triggered three credit checks in rapid succession. This pattern is a red flag for lenders. The borrower may get approved, but at a worse rate than if they had approached the right lender from day one.

The right sequence:

- Check your CIBIL score and profile before approaching any lender

- Match your profile to the lender category and specific institution most likely to approve you at a competitive rate, without a hard inquiry

- Apply to 1–2 matched lenders simultaneously, not sequentially

Butter Money’s ++Eligibility Check++ does exactly this — it shows you your best-matched offers across 30+ lenders with zero impact on your CIBIL score. Your first application becomes your best application.

Want to understand how CIBIL affects your rate and approval? Read: ++CIBIL Score & Home Loans: All You Need to Know Before You Apply++

How to Decide Which Lender to Approach First

Use this simple decision framework before filling out any application:

One more cost nobody plans for: Apart from your EMI, the actual expense incurred in the purchase of property also depends on stamp duty and registration charges, which differ across states.

Know your total buying cost before you finalise your budget: Use Butter Money’s ++Stamp Duty Calculator++ to get state-specific estimates instantly.

Already a home loan borrower? Use these tools too:

- ++Prepayment Calculator++ — Learn how prepaying an amount of ₹1-2 lakhs will reduce your tenure by years

- ++Overdraft Calculator++ — Understand if a Max Saver type account suits you

Related: ++Become Debt-Free Faster with Smart Prepayments++

FAQs: Bank vs HFC vs NBFC Home Loan India

Q1. Is an HFC safer than an NBFC for a home loan? HFCs are a regulated subcategory of NBFCs, now governed by the RBI (since 2019). Major, listed HFCs like LIC Housing Finance, Bajaj Housing Finance, and PNB Housing Finance are as safe and credible as private banks. Smaller or unlisted NBFCs carry more risk — always check the entity’s RBI registration and credit ratings before applying.

Q2. Can I get a home loan from an NBFC if my CIBIL score is below 700? Yes. Most NBFCs and some HFCs (like Aadhar Housing Finance) will consider borrowers with CIBIL scores between 600–700. Expect to pay a higher interest rate. After 12–24 months of clean repayment, consider a balance transfer to a bank or HFC at a lower rate.

Q3. Do HFCs offer PMAY subsidies? Yes. Most recognised HFCs are registered Central Nodal Agencies (CNAs) for the Pradhan Mantri Awas Yojana – Credit Linked Subsidy Scheme (PMAY-CLSS). Eligible first-time homebuyers can claim an interest subsidy of up to ₹2.67 lakh through both banks and registered HFCs.

Q4. Which is better: a bank or an HFC for a self-employed home loan? For self-employed borrowers, HFCs are generally the better starting point. Banks require clean ITRs and stable declared income. HFCs assess your actual repayment capacity — bank statements, business cash flow, and financial projections — giving self-employed applicants a much stronger chance of approval at a competitive rate.

Q5. What is the current repo rate, and how does it affect home loans in India? The RBI Repo Rate is 5.25% as of April 2026 (held unchanged at the April 8 MPC meeting). Bank home loans linked to EBLR (External Benchmark Lending Rate) move directly with the repo rate at each reset cycle (typically every 3 months or as per the loan agreement). HFC and NBFC rates are linked to internal PLRs and may not transmit RBI rate changes as quickly.

Q6. What happens to my EMI if I switch from an NBFC to a bank? Your EMI typically falls meaningfully, sometimes by ₹2,000–5,000/month on a ₹50 lakh loan, because bank rates are 1–3% lower than most NBFC rates. The switch involves a balance transfer process with processing fees (typically 0.5–1%). Use the ++Balance Transfer Calculator++ to calculate if the savings justify the switch for your specific loan.

Q7. Do banks charge a prepayment penalty on home loans? No. As per RBI mandate, banks cannot charge foreclosure or part-payment penalties on floating-rate home loans to individual borrowers. This applies to all scheduled commercial banks. For HFCs and NBFCs, most have also removed prepayment charges, but always verify in the loan agreement before signing.

Related: ++RBI’s No Foreclosure Penalty Guideline 2026: What Every Home Loan Borrower Must Do This Month++

The Bottom Line

Selecting the lender among banks, HFCs, and NBFCs should not be based on how big the institution is, but on finding out which institution suits your profile. Making the wrong choice may mean that you incur high interest rates for a lifetime, or even suffer a reduction in your CIBIL score before being approved.

This is where Butter Money steps in. Rather than approaching multiple institutions and undergoing numerous hard inquiries, Butter Money will use your data to link you to the most fitting lender, from among 30+ banks, HFCs, and NBFCs, all at a minimal interest rate without harming your CIBIL score.

++→ Check My Offers — Free, Takes Under 2 Minutes++

Butter Money matches your home loan profile to the right lender — across banks, HFCs, and NBFCs — with zero impact on your CIBIL score. We make lenders compete so you win.

++→ Check My Offers: Zero CIBIL Impact, Takes Under 2 Minutes++