Buying a Home Together? What You Need to Know Before Signing a Joint Home Loan in India

This Decision Is Bigger Than the Property

You have found the home. You have done the numbers. And somewhere between the site visit and the bank meeting, someone said, “Apply jointly, you will get a much higher loan.”

They are right. But that is only half the story.

A joint home loan is one of the smartest financial moves a couple or family can make when it is structured correctly. The right joint home loan application can unlock significantly more borrowing power. But when it is not structured well, it can quietly damage the credit profile of someone who never missed a payment, limit future borrowing capacity for years, and create legal complications that no one thought about at the time of signing.

This guide covers both sides: the real joint home loan eligibility numbers, the joint home loan tax benefit that most people underuse, and three joint home loan risks nobody explains before you sign.

What a Joint Home Loan Actually Does to Your Eligibility

Every joint home loan eligibility calculation comes down to one number: how much home loan EMI capacity you have after existing obligations. Banks cap this at 50–55% of your monthly income; this is your FOIR (FOIR calculation). When you add a co-applicant home loan, also called a home loan co-borrower, their income enters this calculation directly. The bank assesses combined repayment capacity, which is how you increase the home loan amount without changing the interest rate.

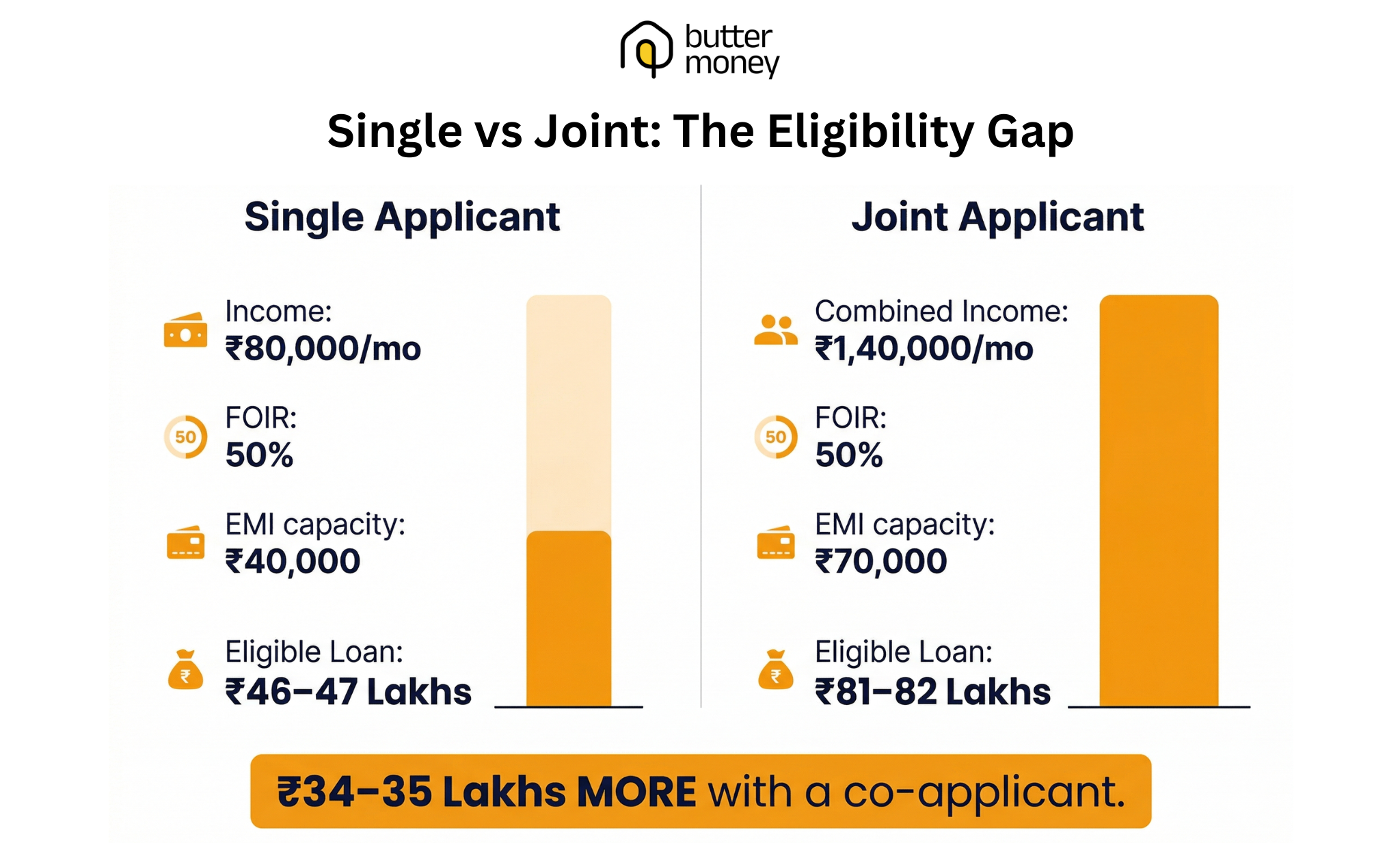

Single vs joint, the eligibility math

Single applicant: Monthly income ₹80,000. No existing EMIs. FOIR calculation at 50% = ₹40,000 available for EMI. At 8.5% for 20 years ≈ ₹46–47 lakhs.

Joint application: joint home loan with spouse: Combined income ₹1,40,000. Same FOIR = ₹70,000 available ≈ ₹81–82 lakhs.

The difference: ₹34–35 lakhs more, same bank, same property, same home loan interest rate.

In Bengaluru’s current market, that gap separates a 2BHK in the periphery from a 2BHK closer to where you actually want to live.

→ Want to run this for your own income numbers? ++Use the Butter Money EMI Calculator++ to model how combined income changes what you can borrow, before any bank conversation.

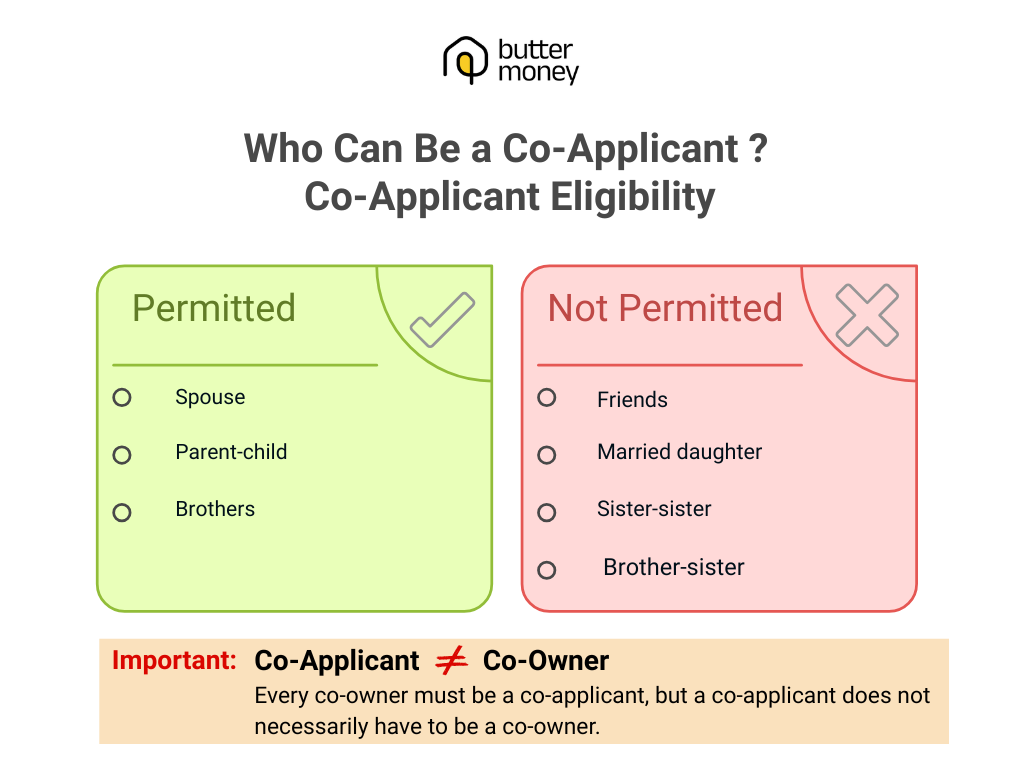

Who Can Be a Co-Applicant and Who Cannot?

This is where most families hit their first surprise. Not every relationship qualifies as a co-applicant home loan in India. Here is a quick reference for your joint home loan documents and lender discussions.

Permitted combinations at most lenders:

- Spouse is the most straightforward and universally accepted combination. Both incomes are clubbed, and joint ownership is clean.

- Parents and children, a father or mother applying with a son, or with an unmarried daughter, are accepted by most banks. Works particularly well when a parent has a stable pension income, or the child is early in their career with a long remaining working tenure.

- Brothers applying together is permitted at several lenders, provided both are co-owners of the property and intend to reside together. This is evaluated case by case and is not universal.

Combinations that most lenders do not permit:

Friends cannot be co-applicants, regardless of shared finances. A married daughter and her parents are typically declined; the concern is ownership clarity post-marriage. Sister-sister or brother-sister combinations are not accepted at most banks unless specific co-ownership conditions are met.

One distinction that matters and is consistently misunderstood: a co-applicant does not automatically become a co-owner. Understanding the co-owner vs co-applicant difference is critical. Every co-owner must be a co-applicant, but you can be a co-applicant without owning the property. This distinction becomes crucial for joint home loan tax benefit and home loan tax deduction claims, which the next section explains.

The Tax Benefit That Most Joint Borrowers Are Not Claiming Fully

This is the part of a joint home loan in India that is most consistently underused, and it compounds across the full tenure. The joint home loan tax benefit is effectively doubled when both co-applicants are registered co-owners.

When both are co-owners, each can independently claim:

- Section 80C home loan deduction: Up to ₹1.5 lakh per year on principal repayment.

- Section 24(b) deduction: Up to ₹2 lakh per year on interest paid (self-occupied property).

For a single applicant, the max annual home loan tax deduction = ₹3.5 lakh. For a joint home loan with both as co-owners, the combined maximum = ₹7 lakh (₹3.5L each).

What this means in real terms:

On the ₹80 lakh joint loan, interest paid in year 1 ≈ ₹6.7 lakhs. Each co-applicant claims ₹2 lakh under Section 24(b), for a combined ₹4 lakh deduction. At 30% bracket, the household saves approximately ₹1.2 lakh in taxes annually, versus a single applicant saving ₹60,000.

The condition: both must be registered co-owners, and each must be contributing to EMI repayment from their own account. A home loan co-borrower who is not a co-owner cannot claim these deductions — regardless of what the loan agreement says.

→ Our home loan tax benefits guide walks through all three sections, 80C, 24(b), and 80EEA, with examples.

→ ++butter.money/blog/posts/home_loan_tax_benefits_blog++

Three Things Nobody Explains Before You Sign

These are the most searched joint home loan risks and the ones most lenders gloss over.

1. Both CIBIL scores go on the loan, and both are affected by every EMI

When a joint home loan CIBIL score is registered, it appears on the credit report of both applicants. Every missed or delayed payment affects both CIBIL scores simultaneously. A co-applicant who has never defaulted in their life can see their score drop because of the primary borrower’s financial difficulty, and they have no way to separate themselves without a loan restructuring or full home loan prepayment joint clearance.

This also means the co-applicant’s debt-to-income ratio changes from day one. If your spouse is the co-applicant on a ₹80 lakh loan, and they later want to apply for a business loan or a personal loan, that ₹80 lakh liability appears on their credit profile. Lenders will factor it into their FOIR calculation.

→ Understanding this before signing prevents surprises later.

++→ butter.money/blog/posts/cibil-score-home-loans-info++

2. Removing a co-applicant from an existing loan is difficult

Life changes. Relationships change. But to remove co-applicant home loan mid-tenure, you need to either refinance the home loan entirely, prove sufficient standalone repayment capacity, or go through a formal legal process that most banks require to be documented. It is not a simple form submission.

Plan the co-applicant decision as if the arrangement will remain in place for the full tenure.

3. Adding a co-applicant after sanction is not straightforward either

If you took the loan as a sole applicant and now want to add a co-applicant to improve repayment capacity or refinance at a better rate, most banks treat this as a modification to the loan structure, not a simple addition. It may require a new application, fresh documentation, and in some cases a new credit assessment. The process is possible but involves more friction than most borrowers expect.

).png)

When a Joint Home Loan May Not Be the Right Move

Adding a co-applicant home loan improves joint home loan eligibility, but not always. Here is when the myths do not work in your favor:

- Low-CIBIL co-applicant: A weaker joint home loan CIBIL score on the co-applicant can pull the combined assessment down, resulting in a higher home loan interest rate, joint or outright rejection.

- Income already sufficient: If the primary borrower’s income meets the requirement comfortably, adding a co-applicant locks someone into a liability without proportionate benefit. The joint home loan tax benefit is real, but must be weighed against credit exposure.

- High FOIR co-applicant: If the home loan co-borrower has existing loans that already consume their FOIR, adding them may not increase home loan amount as expected; banks net out existing obligations first.

→ Here is how to read and improve your eligibility profile before deciding which route to take.

++→ butter.money/blog/posts/know_unlock_eligibility++

Why Lender Choice Matters More on Joint Applications

Not all lenders assess joint home loan eligibility the same way. Some banks apply stricter rules on relationship eligibility; for instance, a parent-child joint home loan application may sail through at one lender and face documentation hurdles at another. Spread calculations, home loan co-borrower income treatment for self-employed profiles, and ownership structure requirements all vary.

At Butter Money, we assess both applicants’ profiles together, income, CIBIL score, FOIR calculation, relationship type, property location, and match the combined profile to lenders where joint home loan India applications are processed most favorably. For most families, the right lender for a home loan for couple in India is not the same as the right lender for a solo one.

→ Applying together? Check your combined eligibility across 40+ lenders on Butter Money.

→ ++Free, instant, and without affecting either applicant’s CIBIL score.++

FAQ

Q1. Who can be a co-applicant in a home loan in India?

Permitted co-applicants include your spouse, parents (with son or unmarried daughter), and brothers (if co-owners). Friends, married daughters, and distant relatives are not accepted at most lenders. Rules vary by bank; some lenders are stricter on parent-child or sibling combinations than others.

Q2. Can I apply for a joint home loan with a non-working spouse?

Yes, but a non-working spouse’s income will not be counted toward eligibility. Their inclusion still helps with co-ownership for tax benefits, but it will not increase the loan amount. If the co-applicant has no income, the bank calculates eligibility based on the primary borrower’s income alone.

Q3. Can both applicants claim tax benefits on a joint home loan?

Yes, provided both co-applicants are also registered co-owners of the property and each contributes to EMI repayment from their own account. Each can claim up to ₹1.5L under Section 80C (principal) and ₹2L under Section 24(b) (interest), doubling the household’s total tax benefit to ₹7L annually.

Q4. Should I apply for a joint home loan if my co-applicant has a low CIBIL score?

No, if the co-applicant’s score is significantly lower than yours, their inclusion can pull the combined credit assessment down, leading to a higher interest rate or loan rejection. In this case, applying as a sole borrower with a strong individual profile is the safer approach. A co-applicant with a score below 700 is generally considered a risk flag by most lenders.

Q5. Can a co-applicant be removed from a home loan mid-tenure?

Yes, but it is not simple. The primary borrower must prove they can repay the loan independently, after which the bank may allow removal through loan refinancing or a formal legal process. It is not a form submission; most banks require fresh documentation and a new credit assessment before releasing the co-applicant.

Explore more:++Understanding Your Home Loan Eligibility++ |++CIBIL Score & Home Loans++ |++Home Loan Tax Benefits++ |++EMI Calculator++